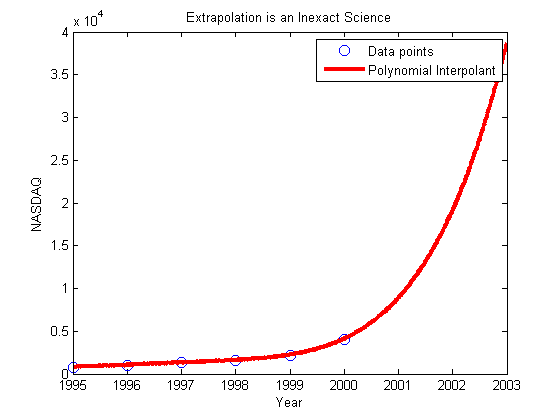

The NASDAQ was booming – people were dreaming of riches – early retirement and what not. The year was 1999 and NASDAQ was at an all time high of 4069 on the last day of 1999.

Yes, Prince was right, not just about the purple rain, but – “‘Cuz they say two thousand zero zero party over, Oops out of time, So tonight I’m gonna party like it’s 1999 party like 1999.”

But as we know the party did not last too long. The dot com bubble burst and as we know it today (June 2008), the NASDAQ is hovering around 2400.

Year ………………NASDAQ on December 31st

1994………………………… 751

1995 ……………………….1052

1996 ………………………..1291

1997 ………………………..1570

1998 ………………………..2192

1999 ………………………..4069

• End of Year NASDAQ Composite Data taken from www.bigcharts.com

So how about extrapolating the value of NASDAQ to not too far ahead – just to the end of 2000 and 2001. This is what you obtain from using a 5th order interpolant for approximation from the above six values.

End of Year …Actual Value …..5th Order Poly Extrapo……………Abs Rel True Error

2000 ……………..2471…………………. 9128 ………………………………….. 269%

2001………………1950……………….. 20720 ………………………………….. 962%

Do you know what would be the extrapolated value of NASDAQ on June 30, 2008 -a whopping 861391! On June 30, 2008, compare it with the actual value.

This post is brought to you by Holistic Numerical Methods: Numerical Methods for the STEM undergraduate at http://nm.mathforcollege.com